Insurance is meant to protect your financial future. But many people unknowingly carry policies with coverage gaps that only become obvious after a claim occurs. In Michigan, the insurance system is also unique because of our No-Fault law, which changes how injuries and vehicle damage are handled after an accident. Because of this, certain coverage mistakes can become extremely expensive. Below are five common insurance mistakes we see, along with real-world style examples that show how quickly costs can add up.

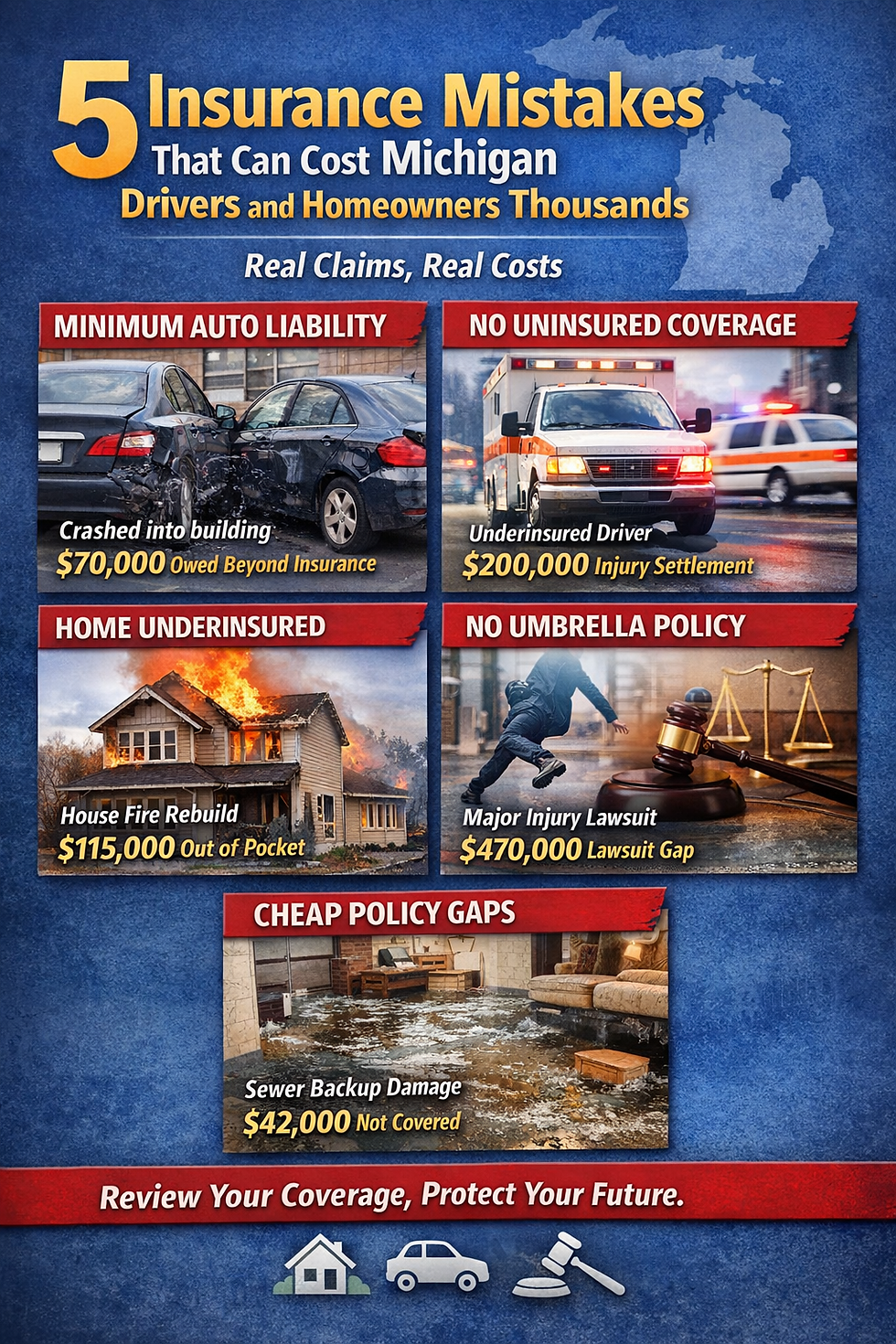

Mistake #1 Carrying Only Minimum Liability Coverage

Many drivers assume that because Michigan is a no-fault state, liability coverage is less important. But liability coverage can still come into play in several situations.

For example, liability coverage may apply if:

• Someone sues for serious impairment of body function

• Property damage occurs outside Michigan

• You damage property other than vehicles (buildings, fences, etc.)

Example Claim

A Michigan driver lost control on icy roads and crashed into a storefront.

Damage to the building: $85,000,Damage to exterior signage and equipment: $22,000, Cleanup and structural repairs: $13,000

Total property damage: $120,000

The driver carried only $50,000 in property damage liability.

Insurance paid: $50,000. Remaining amount owed by the driver: $70,000

Many drivers don’t realize that accidents involving buildings or other structures can create very large liability claims.

Mistake #2 Skipping Uninsured / Underinsured Motorist Coverage

Michigan’s no-fault system means your Personal Injury Protection (PIP) covers medical expenses after an accident, regardless of who caused it. However, uninsured and underinsured motorist coverage protects something different: pain and suffering claims when another driver causes serious injury.

Example Claim

A driver was hit by a vehicle that ran a red light. The injured driver suffered a serious back injury requiring surgery. Medical bills were covered by their PIP coverage. However, they also pursued a pain and suffering claim against the at-fault driver.

Total settlement value for pain and suffering: $250,000

The at-fault driver carried only $50,000 in bodily injury liability.

Because the injured driver carried $250,000 in underinsured motorist coverage, their own policy paid the remaining $200,000.

Without that coverage, the settlement would have been limited to the other driver’s $50,000 policy.

Mistake #3 Insuring Your Home for the Wrong Rebuild Value

Many homeowners believe their house should be insured for what it could sell for on the market. But insurance works differently. Home insurance is based on rebuild cost, not market value.

Example Claim

A kitchen fire spread through a large portion of a home.

Structural rebuild costs: $295,000, Smoke and water remediation: $45,000, Debris removal: $18,000, Temporary living expenses during rebuild: $32,000

Total claim: $390,000

The structure had been insured for only $275,000.

Insurance paid: $275,000. Remaining rebuilding costs: $20,000.

Construction costs and materials often increase faster than home values, which is why periodic coverage reviews are important.

Mistake #4 Not Having Umbrella Liability Coverage

Umbrella policies provide an additional layer of liability protection above home and auto policies. They are particularly important when someone is sued after a serious accident.

Example Claim

A driver caused an accident that resulted in a severe injury meeting Michigan’s serious impairment threshold, allowing the injured party to file a lawsuit for pain and suffering. Settlement for pain and suffering: $650,000, Legal costs: $70,000.

Total liability exposure: $720,000

The driver carried $250,000 in bodily injury liability.

Insurance paid: $250,000

Because the driver also had a $1,000,000 umbrella policy, the remaining $470,000 was covered.

Without the umbrella policy, that difference could have become the driver’s personal responsibility.

Mistake #5 Choosing Insurance Based Only on Price

The lowest-priced policy can sometimes leave out important protections.

Example Claim

During heavy rain, a homeowner experienced a sewer backup that flooded their finished basement. Flooring, drywall, and cabinets: $21,000,Furniture and electronics: $13,000,Cleanup and restoration: $8,000

Total damage: $42,000

The homeowner had selected a lower-cost policy that did not include sewer backup coverage.

Insurance payment: $0 Out-of-pocket cost: $42,000

Adding sewer backup coverage would typically cost less than $100 per year depending on the policy.

Insurance is not just about finding the lowest premium. It is about protecting your home, your savings, and your financial future.

Small differences in coverage can make a very large difference when a claim occurs. Taking time to review your coverage regularly helps ensure your protection keeps up with your life — and can prevent very expensive surprises later.

Comments